Stock-based compensation can be a valuable part of your overall pay package, but it frequently comes with tax complexities. While equity awards can help build capital over time, a lack of planning often leads to surprising tax liabilities. Knowing how and when different types of stock compensation are taxed is important to making well-informed financial decisions.

If you receive stock compensation, understanding the tax implications up front helps avoid costly surprises. This guide breaks down tax rules and reporting for NSOs, ISOs, RSUs, and ESPPs so you can plan with confidence.

What Is Stock Compensation?

Stock compensation is a form of non-cash pay tied directly to company equity. Employers use it to attract, retain, and motivate employees by aligning their financial interests with the business’s long-term success. However, the way these awards work—and how they are taxed—varies widely depending on the type of award.

Some awards give you the right to purchase shares at a fixed price, while others deliver shares after vesting. These differences directly affect when taxes are triggered and how the income is treated.

The Four Main Types of Stock Compensation

-

-

NSOs (Non-Statutory Stock Options): The right to buy shares at a fixed price

-

ISOs (Incentive Stock Options): Employee-only stock options with potential tax advantages

-

RSUs (Restricted Stock Units): The company promises to grant shares once the vesting criteria is met.

-

ESPPs (Employee Stock Purchase Plans): Plans that let employees buy company stock, often at a discount, through payroll deductions.

-

When Is Stock Compensation Taxed?

Stock compensation typically triggers taxation in two stages:

1. Compensation-related event: When you first realize value, such as exercising options or RSUs vesting.

2. Investment-related event: When you sell the shares and generate a capital gain or loss.

Four key timing questions apply to nearly any equity award:

1. Is it taxed at grant, when the company awards the equity?

2. Is it taxed at vesting, when you earn the right to the equity?

3. Is it taxed at exercise or purchase when you acquire the shares?

4. Is it taxed at sale, when you sell the stock?

Ordinary Income vs. Capital Gains

The nature of the tax can change as you move through the lifecycle of an award.

When you first realize value through vesting, exercise, or purchase, the IRS generally treats that value as ordinary income. Later, when you sell your shares for more or less than your tax basis, the difference is generally treated as capital gains or capital loss.

In some cases, there may also be additional considerations. For example, exercising ISOs may create exposure to the Alternative Minimum Tax (AMT) even if you do not sell the shares right away.

How Non-Statutory Stock Options (NSOs) Are Taxed

Non-statutory stock options are one of the most common forms of stock options and have relatively straightforward tax treatment.

What are NSOs?

NSOs give you the right to buy a set number of company shares at a fixed price, known as the strike price or exercise price. They do not meet requirements for special treatment, so they follow standard compensation tax rules.

When are NSOs taxed?

NSOs are typically not taxed when granted, and vesting generally does not trigger a taxable event.

NSOs are usually taxed when you exercise the option. The difference between the strike price and fair market value (the “spread”) is taxed as ordinary income and subject to payroll taxes.

Any later appreciation or decline in the stock's value is generally treated as a capital gain or capital loss when the stock is eventually sold.

Example: You exercise 1,000 NSOs with a $10 strike when the stock is worth $50. The $40 per-share spread creates $40,000 of ordinary income. Later, if the shares are sold at $70, the additional $20 per share ($20,000) is generally a capital gain.

Planning Tip: Consider exercising in years when your income is lower to help manage your tax rate. Also, keep in mind that employer withholding at exercise may not fully cover your full tax liability.

How Incentive Stock Options (ISOs) Are Taxed

Incentive stock options can offer more beneficial tax treatment than NSOs, but they come with stricter holding rules and added complexity.

What are ISOs?

ISOs are statutory stock options for employees. Special tax rules and holding-period requirements determine whether your profit is taxed as ordinary income or capital gain.

There is also an annual $100,000 rule to keep in mind. In general, no more than $100,000 based on the fair market value at the time the option was granted, can first become exercisable in a single calendar year and still retain ISO treatment. Amounts above that limit are generally treated as nonqualified options for tax purposes.

When are ISOs taxed?

Like NSOs, ISOs are generally not taxed at grant. Unlike NSOs, qualifying dispositions are not subject to regular tax at the time you exercise your stocks.

However, exercising an ISO may trigger the AMT. For many employees, the primary tax consequences arise when the shares are eventually sold.

Qualifying vs. disqualifying dispositions

To receive an advantageous tax treatment, the sale must meet the rules of a qualifying disposition. That means holding the shares for at least:

-

-

two years after the grant date, and

-

one year after the exercise date

-

If you sell too early, before meeting those requirements, the sale is considered a disqualifying disposition. In that case, part of the gain is generally treated as ordinary income, negating the ISO’s main tax advantage.

While income from a disqualifying disposition is generally reported as wages on Form W-2, it typically is not subject to Social Security or Medicare tax withholding.

Why AMT matters with ISOs

The Alternative Minimum Tax is a separate tax calculation designed to ensure high earners pay a minimum amount of tax. When you exercise ISOs and hold the shares, the spread between the strike price and the fair market value will be included as AMT income on Form 6251 for that year.

That means you could face a tax bill even if you have not sold the stock or received cash from the transaction. AMT is one of the biggest planning considerations with ISOs.

AMT paid because of ISO timing differences may create a minimum tax credit that can potentially be used in future years. That credit can also become part of the planning discussion when deciding whether to continue holding shares or sell sooner.

Example 1: Qualifying disposition

You exercise ISOs with a $10 strike price when the stock is worth $50. There is no regular income tax at exercise, but the $40 per-share spread may trigger an AMT adjustment. If you later sell shares at $70 after meeting the holding requirements, the $60 per share total gain may qualify for long-term capital gains treatment.

Example 2: Disqualifying disposition

You exercise ISOs at $10 when the stock is worth $50, then sell the shares later at $55 before meeting the holding requirements. In general, the bargain element, up to the $40 spread at exercise, is treated as ordinary income. Any remaining gain may be treated as capital gain.

Planning Tip: Consider AMT impact before exercising ISOs, especially if you plan to hold the shares. Timing can make a difference. Exercising earlier in the year may give you enough time to satisfy the one-year holding period before the following tax deadline, which can make it easier to plan for any tax due. Another approach is the “AMT crossover” strategy, which involves exercising only enough options to remain below the AMT threshold. And with private-company options, exercising before a major valuation increase or before an IPO may help limit AMT exposure.

How Restricted Stock Units (RSUs) Are Taxed

RSUs are increasingly popular because they retain value as long as the stock trades above zero. Their tax treatment is fairly straightforward, but many employers still underestimate the tax impact.

What are RSUs?

An RSU is a promise from your employer to deliver shares upon meeting specific vesting conditions, such as a set period of employment or performance goals.

When are RSUs taxed?

RSUs are typically not taxed when granted. They are usually taxed when they vest and the shares or cash value become available to you.

At vesting, the fair market value of the shares is generally treated as ordinary income. Any gain or loss after the vesting date is generally treated as a capital gain or capital loss when the shares are sold.

Why withholding can still leave a gap

When RSUs vest, employers typically withhold shares or cash to cover taxes. For federal income tax purposes, supplemental wages are generally withheld at a flat 22% rate for amounts up to $1 million during the calendar year and generally increases to 37% on supplemental wages above that threshold.

However, the withholding amount may not fully reflect your actual tax liability, particularly if you are a high earner or subject to additional state taxes.

As a result, some employees receive a tax bill at filing time even though withholding occurred at vesting.

Example: 1,000 RSUs vest when the stock is worth $50, creating $50,000 of ordinary income. Your employer withholds some shares or cash for taxes. If you sell the remaining shares later at $60, the $10 per-share gain is generally a capital gain.

Planning Tip: Treat an RSU vest like a taxable bonus. To reduce risk and simplify planning, consider selling shares at vesting rather than holding a large position in company stock.

How Employee Stock Purchase Plans (ESPPs) Are Taxed

ESPPs allow employees to buy company stock, often at a discount, with tax treatment depending on how long they hold the shares.

What is an ESPP?

An ESPP lets employees buy company stock, often at up to a 15% discount, via payroll deductions.

When are ESPPs taxed?

ESPPs are generally not taxed at grant. Under a qualified ESPP, they are also often not taxed at purchase. Tax consequences generally arise when the shares are eventually sold.

Like ISOs, ESPPs can receive more favorable treatment if the holding period requirements are met. In general, a qualifying disposition requires that you hold the shares for at least two years from the grant or offering date and one year from the purchase date. If you sell before meeting those rules, the sale is generally a disqualifying disposition, and more of the gain may be taxed as ordinary income rather than capital gain.

Example: You purchase shares at $85 when the FMV is $100. If you sell immediately, the $15 discount is generally taxed as ordinary income. If you hold the shares long enough to meet the qualifying disposition, more of your total profit may qualify for capital gains treatment.

Planning Tip: Weigh the value of the purchase discount versus market risk, concentration risk, and cash flow. It is also important to keep track of purchase dates, prices, and cost basis.

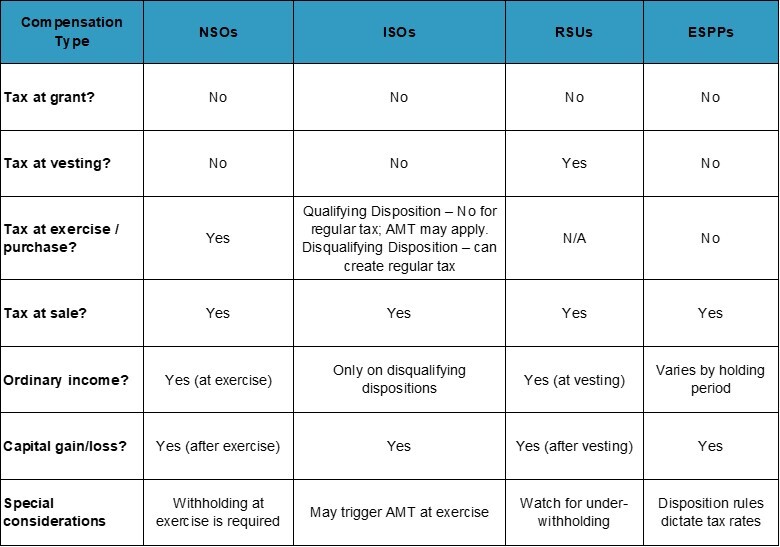

Tax Comparison Table

Tax treatment can vary widely depending on the timing and type of award. Reviewing your options with a tax advisor before you exercise or sell can help you avoid tax liabilities down the road.

Capital Gains, Capital Losses, and Cost Basis

After acquiring shares, your cost basis is equal to what you paid plus any income amount already taxed as ordinary income. Future appreciation may be subject to capital gains tax when sold. If the value drops below the cost basis, you may claim a capital loss.

-

-

Short-term capital gains: Apply when shares are held one year or less and are taxed at ordinary income rates.

-

Long-term capital gains: Apply when shares are held more than one year and are taxed at lower rates.

-

Why Cost Basis Matters

Cost basis is the starting point for measuring gain or loss on a stock sale. Properly tracking it is critical because part of the stock’s value may have already been taxed as compensation.

If the basis is reported incorrectly, you end up paying twice on the same income or overstating your capital gain. Coordinating stock sales with advanced strategies, such as tax-efficient investing and tax-loss harvesting, can improve your overall tax outcome.

What Tax Forms Are Used?

Reporting stock compensation often requires filing several IRS forms, including:

-

-

Form W-2: Reports compensation income from RSU vesting, NSO exercises, and disqualifying ESPP sales.

-

Form 1099-B: Issued by your brokerage for the sale of stock.

-

Form 3921: Reports ISO exercises.

-

Form 3922: Reports ESPP purchases or transfers.

-

Form 8949: Reports capital gains, losses, and cost basis adjustments.

-

Schedule D: Summarizes capital gains and losses on your tax return.

-

Form 6251: Used to calculate the Alternative Minimum Tax.

-

Common Errors: One of the most frequent issues is failure to adjust cost basis correctly. Before filing, review your Form 1099-B and confirm that any amount already taxed as ordinary income is reflected appropriately. Inaccurate reporting can lead to overpayment or trigger IRS notices.

Avoiding Common Tax Mistakes

Some of the most frequent errors with equity compensation include:

-

-

Exercising options without understanding the immediate tax impact and being unprepared for the IRS bill.

-

Failing to diversify and accruing too much company stock.

-

Underestimating tax due because of insufficient withholding on RSUs.

-

Overlooking AMT exposure on ISOs.

-

Misreporting the sale of stock for failing to correct the cost basis.

-

Misunderstanding the rules for ESPP qualifying versus disqualifying sales.

-

Bonus planning considerations: While it does not apply to every compensation covered here, some taxpayers may also want to consider a Section 83(b) election. This election lets you choose to be taxed on certain nonvested stock up front instead of waiting until it vests, which can be beneficial if the value is still low and you expect it to grow. But it also carries risks. If the stock drops in value or is forfeited, you may not get that tax back. For founders and early employees, it may make sense to consider whether shares may eventually qualify for Section 1202 QSBS treatment, depending on the company and stock structure.

The best way to avoid these issues is to stay proactive. Track your awards carefully, understand the tax triggers for each type of compensation, and seek professional advice where needed. For executives and other insiders, Rule 10b5-1 plans can also be a useful planning tool when setting up stock sales in advance. These decisions often play a part in broader HNWI tax planning and long-term tax-efficient investing.

When to Consult a Tax Advisor

Tax planning for equity compensation is often outside the scope of standard DIY tax prep. It may make sense to work with a professional if:

-

-

You have multiple types of equity awards.

-

You expect a significant vesting, exercising, or liquidity event.

-

You face possible AMT exposure.

-

You have concentrated holdings in company stock.

-

You moved states during the vesting or exercise period and may need to determine how stock compensation should be allocated between states

-

You want to integrate equity decisions with your overall tax and wealth strategy.

-

A proactive plan can help reduce surprises, improve compliance, and make the most of the wealth-building opportunities of your equity compensation.

Make Informed Decisions With Your Equity

Stock compensation can be a powerful wealth-building tool, but it comes with complex tax rules and planning considerations. Each type of award is taxed differently, and understanding the tax consequences can help you avoid costly mistakes and make better decisions.

If you receive equity compensation, talk to an LTax advisor before filing, exercising, or selling. We’re here to help you create a personalized plan to make sure your stock compensation supports your broader tax strategy and long-term wealth goals.

FAQs

How is stock compensation taxed?

Stock compensation is taxed based on the type of award and what you do with it. Typically, there are two phases: first, ordinary income tax when you realize compensation value, and later, capital gains tax when you sell the shares.

How do ISOs differ from NSOs?

Unlike NSOs, ISOs do not trigger regular ordinary income tax at exercise. If the required holding periods are met, more of the gain may qualify for long-term capital gains rates. However, exercising ISOs can create AMT exposure.

Are RSUs taxed at 40%?

RSUs are not automatically taxed at 40%. When RSUs vest, their value is taxed as ordinary income based on your applicable tax rates. Depending on your total income level and state taxes, your combined rate could approach 40% or more, but there is no universal RSU tax rate.

Do I pay capital gains tax on stock compensation?

Yes. Once you acquire shares, any future appreciation above your cost basis is subject to capital gains tax when you sell. Holding the shares for more than one year qualifies you for lower long-term capital gains rates.

Consult an LTax team member today to explore ways to understand the tax implications and avoid costly surprises.

LEGAL OR TAX: The information herein is not legal, such as trust or estate planning, advice, or tax advice. Any such information is provided for illustrative purposes only and must not be relied upon without the benefit of the advice of your lawyer and/or tax professional. Lido specifically disclaims any liability from any reliance on such information. Lido is not a legal service provider or tax professional and does not offer legal or tax advice. Should you desire to obtain tax or legal services or advice, you must enter into your own, independent engagement agreement with a licensed attorney or tax professional.