Key Takeaways

-

HELOC interest is only deductible if funds are used to buy, build, or substantially improve your home.

-

SBLOC funds generally cannot be used to buy securities, and they are not tax-deductible.

-

Claiming investment interest expense requires Form 4952 and thorough record-keeping

-

Borrowing against a portfolio (Margin/SBLOC) introduces the risk of forced liquidation if asset values drop.

For high-net-worth individuals and investors, the need for liquidity frequently arises at inconvenient times. Whether you need cash for a tax bill, a real estate opportunity, or a major renovation, the choice often comes down to a margin loan, a Home Equity Line of Credit (HELOC), or a Securities-Backed Line of Credit (SBLOC). Each of these common investing tools has unique tax implications and plays a particular role in a holistic tax strategy and wealth plan.

Selling highly appreciated stocks, bonds, or real estate can trigger unwanted capital gains taxes, shrinking your long-term portfolio value. Asset-backed borrowing provides a savvy alternative, unlocking capital for new investments, diversification, or estate planning without an immediate taxable event.

In this guide, we break down the tax implications, financial planning considerations, and risks of margin loans, HELOCs, and SBLOCs.

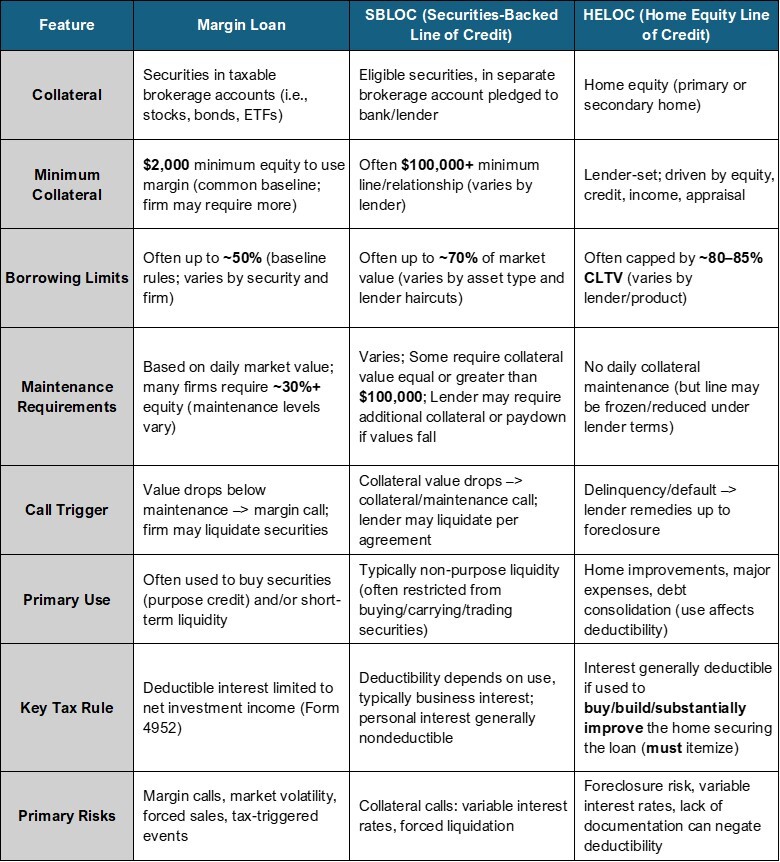

Margin Loan vs HELOC vs SBLOC: Asset-Backed Borrowing at a Glance

Note: Numbers below reflect common baselines and typical ranges. Brokers and banks often apply stricter requirements based on collateral type, concentration, and market variability.

Margin Loan vs HELOC vs SBLOC: Tax Considerations and Planning Home Equity Line of Credit (HELOC)

A HELOC allows homeowners to borrow against the equity in their residence. Unlike a standard mortgage, it is a revolving line of credit with a draw period (typically 10 years) followed by a repayment period.

How it works

Banks typically lend up to 80% or 85% of your home's appraised value, minus what you owe on your primary mortgage. Because the loan is secured by real estate, interest rates are often lower than those of unsecured personal loans, though they are usually variable.

Tax implications

The passage of the One Big Beautiful Bill Act (OBBBA) permanently extended the Tax Cuts and Jobs Act (TCJA) stricter rule on deducting HELOC interest. Now, you can only deduct interest on home equity debt if both of the following apply:

- The loan is secured by your qualified main home or second home.

- The proceeds are used to buy, build, or substantially improve the property used as collateral.

Using HELOC funds to pay off credit card debt, cover tuition, or purchase a vehicle renders the interest nondeductible. Furthermore, the deduction is limited to interest on up to $750,000 of combined qualified residence debt ($375,000 if married filing separately).

Important Note: To claim this deduction, you must itemize on Schedule A rather than taking the standard deduction.

Best for: Real estate investors and homeowners looking for tax-advantaged financing for home improvement projects or property upgrades.

Margin Loans

A margin loan involves borrowing money from a brokerage firm using the securities in your portfolio as collateral. Although frequently used by traders to buy more stock (leverage) or defer asset sales, margin loans can also be used for short-term liquidity needs.

How it works

This is a "purpose" credit under regulatory definitions when used to buy securities. The loan is tied to a designated brokerage account. If the value of your portfolio drops below the broker’s maintenance requirement, a "margin call" may be issued. A margin call requires you to deposit cash or sell a portion of your portfolio assets immediately.

Tax implications

If you use margin proceeds to purchase taxable investments, the interest is classified as "investment interest expense." This is generally tax-deductible, but with specific limitations:

- Net Investment Income Cap: You can only deduct investment interest up to the amount of your net investment income (e.g., ordinary dividends, interest income) for the year.

- Carryforward: If your interest expense exceeds your investment income, the disallowed portion can be carried forward to future tax years.

- Form 4952: To claim the investment expense deduction, you must file IRS Form 4952.

- Tax-Exempt Exception: Margin loans used to purchase tax-advantaged or tax-exempt securities (i.e., municipal bonds) are not eligible for interest deduction.

Best for: Active investors and financial planners who use asset leverage for diversified portfolio building or tax deferral.

Securities-Backed Line of Credit (SBLOC)

An SBLOC is a bank loan secured by your investment portfolio, but it differs from margin lending. It is a "non-purpose" loan, meaning regulations prohibit using the proceeds to purchase or carry margin stock.

How it works

SBLOCs are designed for liquidity. You might use an SBLOC to pay a large tax bill, finance a bridge loan for real estate, or cover a business expense. Because you cannot use the funds to double down on stocks, the risk profile differs slightly from margin. Although forced liquidation is still a risk if your portfolio value collapses.

Tax implications

The tax treatment of SBLOC interest depends entirely on how you spend the money (known as interest tracing). For the vast majority of individuals using SBLOCs for lifestyle cash flow, there is no tax deduction available.

- Personal Expenses: If you use the funds for a wedding, vacation, or car, the interest is classified as personal interest and is nondeductible.

- Business Expenses: If the funds are used for a trade or business expenditure, you may be able to deduct the interest.

- Investment Expenses: You cannot use SBLOCs to buy further securities. SBLOC investment expenses are not tax-deductible.

Best for: Individuals and investors who need rapid, low-friction funding for financial planning, business needs, or cash flow bridging, while keeping their investment strategy intact.

Using Leverage: Key Tax and Risk Considerations

The "Buy, Borrow, Die" Wealth Strategy

One advanced tax strategy popular with investors is "buy, borrow, die." Instead of selling and paying capital gains tax, you buy appreciating assets and borrow against them for liquidity (using margin loans, HELOCs, or SBLOCs—depending on tax implications). Ultimately, you pass assets to your heirs with a step-up in basis. This can be a powerful estate and legacy planning tool, but it carries market and legal risks.

Portfolio and Collateral Risks

-

Margin and SBLOC: Subject to market swings. A swift drop can trigger a margin or collateral call, forcing the sale of assets at an inopportune (and taxable) time.

-

HELOC: Tied to your real property. Payment failures can result in foreclosure and lost tax advantages.

Interest Rate Risk

Most asset-backed loans, including margin loans, SBLOCs, and HELOCs, have variable interest rates. Understand how shifts in rate environments affect your after-tax cost and cash flow in both the short and long term.

An Integrated Approach to Borrowing and Tax Planning

Asset-backed borrowing provides taxpayers with a way to unlock liquidity without interfering with their investment strategy or triggering immediate tax liabilities. However, choosing between a Margin Loan, HELOC, or SBLOC calls for thorough consideration to avoid serious tax consequences. Planning ahead and establishing a repayment plan from the start is important.

At LTax Consulting, we help clients understand the tax implications of margin loans, HELOCs, and SBLOCs and how customized borrowing strategies can support their financial plans.

Contact an LTax team member today to schedule a consultation and optimize your asset-backed borrowing strategy for tax efficiency and long-term monetary growth.

Frequently Asked Questions

Is margin interest always tax-deductible?

No, margin interest is only deductible if the loan proceeds are used to purchase taxable investments. It is also limited to your net investment income for the year. If you use a margin loan to buy a car, the interest is considered personal and not deductible.

Does borrowing against my portfolio trigger capital gains tax?

Generally, no. Taking a loan against your assets is not considered a sale by the IRS, so it does not trigger capital gains tax. However, if the lender forces a sale of your assets to cover a margin call, that sale is a taxable event.

Can I deduct HELOC interest if I use the proceeds to pay off credit card debt?

No. Under the Tax Cuts and Jobs Act, HELOC interest is only deductible if the funds are used to buy, build, or substantially improve the home securing the loan. Using funds for debt consolidation voids the interest as nondeductible.

What is Form 4952?

IRS Form 4952 (Investment Interest Expense Deduction) is used to calculate the amount of investment interest expense you can deduct in the current tax year and how much must be carried forward. You must file this form if you are claiming a deduction for investment interest.

LEGAL OR TAX: The information herein is not legal, such as trust or estate planning, advice, or tax advice. Any such information is provided for illustrative purposes only and must not be relied upon without the benefit of the advice of your lawyer and/or tax professional. Lido specifically disclaims any liability from any reliance on such information. Lido is not a legal service provider or tax professional and does not offer legal or tax advice. Should you desire to obtain tax or legal services or advice, you must enter into your own, independent engagement agreement with a licensed attorney or tax professional.